Crude Oil: Don’t Hurry To Sell

Over the last month, oil has shown minimum volatility, being supported, on the one hand, by the political crisis in Venezuela and the decline in oil production in OPEC countries and Russia, and on the other hand, being under pressure of concerns about global growth. And today, I offer my forecast regarding the direction in which the market is most likely to move.

First of all, let us recall what OPEC decided in December:

In view of the current fundamentals and the consensus view of a growing imbalance in 2019, the Conference decided to adjust OPEC overall production by 0.8 mb/d from October 2018 levels, effective as of January 2019, for an initial period of six months, with a review in April 2019….

Now, let us recall how much oil OPEC countries produced in October:

As we can see, in October, OPEC oil production was 32.976 mb/d. But this is with account taken of Qatar that left the cartel. Without Qatar, oil production was 32.36 mb/d. We subtract 0.8 mb/d from this figure and we get 31.6 mb/d ‒ this is the target level of OPEC oil production at the end of the second half of the current year. Averaging out, it can be predicted that in Q1, OPEC oil production will be 31.8 mb/d, and in Q2, it will be 31.6 mb/d.

Based on these calculations and the latest OPEC forecast regarding the structure of global supply and demand in the oil market, we obtain the following structure of the oil market global balance for the next six months:

So, judging by the OPEC data, the global oil market is to have a stable surplus for two quarters. Now, let’s estimate what this means for the price of oil. As it turns out, not everything is so obvious here …

In the long run, in the oil market (like any other commodity market), the price is formed on the basis of the balance between supply and demand. One of the markers of this balance is stocks. That is why there is a good long-term relationship (R2 = 0.85) between the price of Brent oil and the OECD commercial closing stock levels:

OPEC publishes oil stock reports for the OECD with one quarter delay. Therefore, we will calculate them on our own. Given that oil consumption by OECD countries is approximately 50% of the global consumption level, it can be assumed that the possible deficit or surplus in the global oil market will be compensated by 50% due to oil inventory in the OECD countries. This means that the expected surplus in the oil market can increase oil stocks in the OECD countries to ~2,950 mb by the end of the second quarter.

As we can see from the model below, it means that the current price of Brent oil almost corresponds to the forecasted level of oil stock in the OECD countries in Q2:

I would like to note that this, in essence, simple model has been serving as a good indicator of the balanced Brent oil price over the past eight years. But this model does not take into account an important element that is demand. And agree that the same level of stocks but with different level of consumption affects the price differently. Therefore, the next step is to consider the relationship between the price of Brent oil and the number of days of forward consumption in OECD (stocks divided by daily oil consumption):

As you see, according to this model, the current price of Brent oil is undervalued by ~$10. In other words, in terms of the expected demand, the expected increase in oil stocks in the OECD will not have a disastrous effect on the price of oil.

As you see, according to this model, the current price of Brent oil is undervalued by ~$10. In other words, in terms of the expected demand, the expected increase in oil stocks in the OECD will not have a disastrous effect on the price of oil.

More than that, if we recalculate everything based on the IEA’s forecast, we will get a very slight surplus in Q1, and almost the same deficit in Q2:

In other words, according to the IEA, global oil stocks will not change significantly in the first half of the year, which, within the bounds of the proposed models, means that the current price of Brent oil is clearly below the balanced level.

Going further. Just like you, I read a lot about the signs of the global economic slowdown led by China (the largest consumer of oil). But here is an interesting fact. So far, these fears have not been reflected in the IEA’s and OPEC’s forecasts regarding oil consumption by the OECD countries this year:

And, they have only led to a very slight decrease in the forecasted global oil demand:

Do not misunderstand me, I do not urge to underestimate the risks of global economic slowdown, I just want to draw attention to the fact that so far, they have not had a considerable impact on global oil consumption. And, let me remind you that the Chinese government is preparing large-scale fiscal incentives in the amount of $370bn to support its economy. Besides, trade negotiations between the US and China are continuing, and in my opinion, both parties are still interested in an agreement.

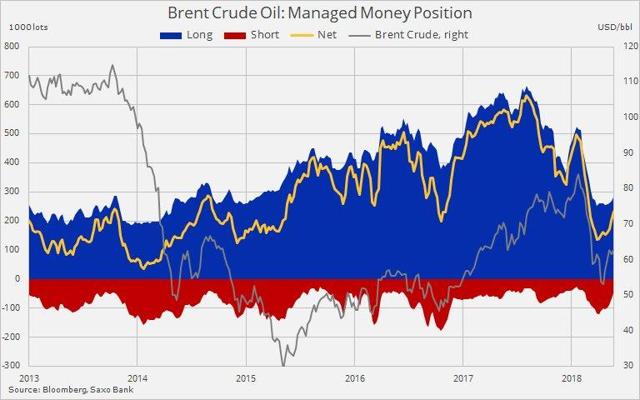

Finally, I would like to address the latest hedge funds’ actions that complement the overall picture. In the week to January 29, hedge funds increased bullish bets on Brent oil by 30 thousand lots to 233 thousand lots. Over the week, they closed 18 thousand previously sold contracts and buy about 12 thousand of new oil contracts:

Bottom line

So, we see that:

- Based on OPEC’s forecasts, in the first half of the year, we can expect an increase in oil stocks in the world and the OECD countries. But in terms of the expected demand, it will not have a disastrous effect on the price of oil.

- The IEA forecasts do not imply growth in oil stocks in the world and the OECD countries over the next 6 months. In this case, the current price of oil may be considered as undervalued.

- Neither OPEC nor the IEA has considerably brought down their forecasts for global oil demand in the current year yet.

- In January, hedge funds actively bought oil.

All these facts mean that it is risky now to sell oil.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Powered by WPeMatico