Kraft Heinz: Be Fearful When Everyone Is Quoting Buffett

When we last touched on The Kraft Heinz Company (KHC) after the results, our key takeaway was that the stock “appeared cheap” and the main problem was significantly bloated forward estimates. Our decision to stay out has so far proven correct as the stock has not been able to find its footing. While we have stayed on the sidelines, we have seen many bullish takes on the stock, replete with Buffett quotes. That makes sense as Warren Buffett owns a substantial stake in this company and is never one to shy away from showering us with a Hallmark card worthy quote.

We have been known to use sentiment a lot in our work. It has produced some great results. It helped us pick among other, the massive lifetime top in NVIDIA (NVDA) and this timely bottom in Altria (MO). Fear and greed play a role in all investments and running the theme on valuation without being cognizant of sentiment is likely to cause significant pain. At the same time, one has to take into account the rather difficult path that lies ahead of KHC. We hope to provide the risks of owning this investment and identify the point at which it does become worth risking your neck for.

KHC, an all you can eat Buffett?

Our initial call on KHC came with the biggest warning on earnings estimates. The numbers from GroupThink were not be trusted.

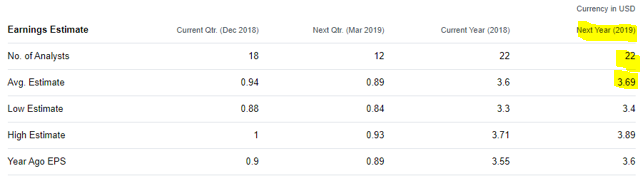

Source: Yahoo Finance before the storm

Source: Yahoo Finance before the storm

22 analysts were clustered around $3.69 cent mark as if it were almost a foregone conclusion. Fast forward to two weeks later and there appears to be a greater appreciation for KHC’s issues, with one analyst moving on to a less challenging profession.

Source: Yahoo Finance

Source: Yahoo Finance

Are these the lowest numbers? We think they are close to bottoming out for sure but the challenge is what happens next.

The real challenge for KHC

On the Q4-2018 conference call we identify the key points that likely spooked money managers to empty their portfolios in the cascade (emphasis ours).

So to be more specific, if you assume the midpoint of our range or a roughly $700 million decline year-over-year, let me elaborate on the four main drivers behind that.

So first off, on the commercial side, again, we should be neutral on the bottom line as we expect the positive contribution from further consumption gains to be in line with the stepped-up investments as we accelerate the pace of our innovation, base business performance and channel development; second, beyond that, roughly half of the total EBITDA decline or roughly $300 million to $400 million is driven by continued inflation, net of cost savings, in the low to mid-single-digit range, consistent with what we saw in 2018. So this will be driven by another year of mid-single-digit growth — low to mid-single-digit growth inflation, excluding key commodities. And given the recent experience, actions we’ve taken to replan the savings and pushing out the savings curve. Third, we expect the combination of foreign exchange headwinds and the divestitures we’ve already announced, that should drive another $250 million headwind to adjusted EBITDA versus 2018. And then, finally, we have an impact from variable compensation, which is another roughly $80 million year-over-year.

That is the key point investors must address. If KHC, suffered mid single digit cost inflation in a year where commodities did this…

Data by YCharts

Data by YCharts

and it expects to continue to suffer in 2019 from high inflation in its component products without offsetting price increases…what happens in a year when commodities go up substantially?

In other words, can we call $2.80 of EPS the trough? A 5% further increase in cost of goods sold without corresponding increases sale prices would decrease gross profits by about 10% and operating income by about 14%. Suddenly the forward P/E is 13 even at this lowered stock price. Investors should bear in mind that three weeks ago the buyer at $47 felt that he was buying the stock at a 13X P/E multiple.

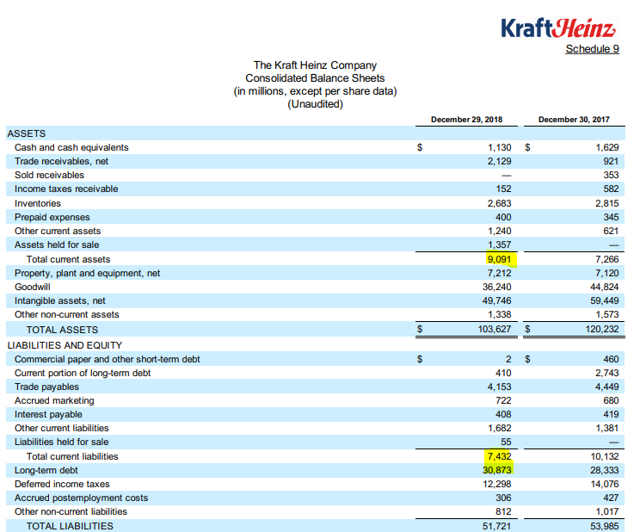

The unbalanced balance sheet

Assuming KHC needs zero working capital over the long run, and the excess can be used to pay off debt, it still has to grapple with $29 Billion of debt versus $6.4 Billion of EBITDA. That is running at 4.55X.

Source: KHC 8-K

It is not extraordinarily high for a consumer staples company, but remember, in 2017, this number was under 4.0X and it is now rising to a point where further increases would be extremely troublesome. Deleveraging is going to be tough as excess cash flow after dividends should be around $1.5 billion annually. It will take more than two years just to bring it back under 4.0X, a point we consider to be the safezone.

Why we have moved to slightly more optimistic stance

We look at P/E ratios after we have looked at everything else as they can be really deceiving near top and bottoms. They can also be deceiving in a leveraged business suffering from a margin collapse. That said, the EV to EBITDA is now moving under 11X. This is getting close to a point where you can stick your neck out and take a stand that this is buy. A lot has to go go right though for this to become a stellar investment again and investors should be cognizant that if KHC has any further hiccups even that $1.60 dividend will fly straight out of the window.

We want to get involved here but with a wider than average margin of safety. At $28/share, the EV to EBITDA will be under 10X, a point we can safely say that risk reward will be firmy in our favor. On our now very famous scale of 1-10, where 1 would be “Avoid like the bubonic plague” and 10 would be “Buy like this is Apple (NASDAQ:AAPL) in March 2009,” we would rate KHC a 5.0, with a $28 price warranting a 6.0. With that in mind, we will be looking at selling the right puts to establish our long position.

Conclusion

Investors should recognize that until KHC shows some semblance of pricing power, it will struggle. We think this can be done but we want to buy with an adequate safety buffer that increases the odds of it working out. Just because there is a high degree of fear, does not automatically make this a good investment. KHC purchase is also violating one of our Oracle’s rules as we are trying to buy a fair company at a wonderful price.

The Wheel of FORTUNE is a most comprehensive service, covering all asset classes: common stocks, preferred shares, bonds, options, currencies, commodities, ETFs, CEFs, etc.

Take advantage of the two-week free trial and gain access to our:

- Monthly Review, where all trades are monitored.

- Trading Alerts. We don’t trade every day, but we issue one trade per trading day, on average.

- Model Portfolio, aimed at beating the S&P 500 performance.

- “Getting Ready For 2019“, a 19-part series, featuring our top picks across eleven sectors plus eight segments.

What are you waiting for?! Time is Money!

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in KHC over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints. Tipranks: HOLD

Powered by WPeMatico